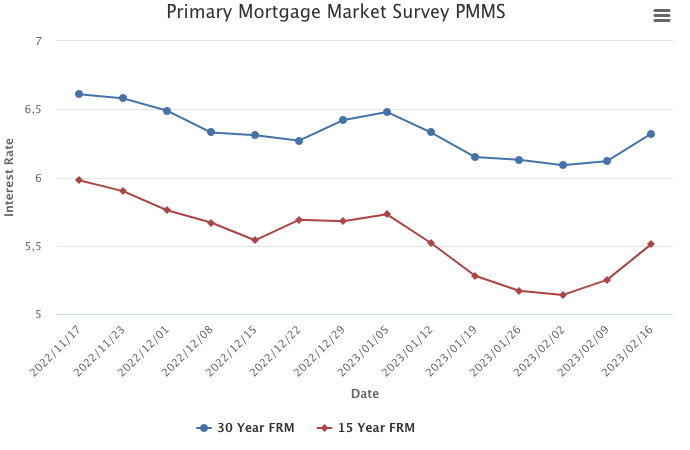

February 16, 2023

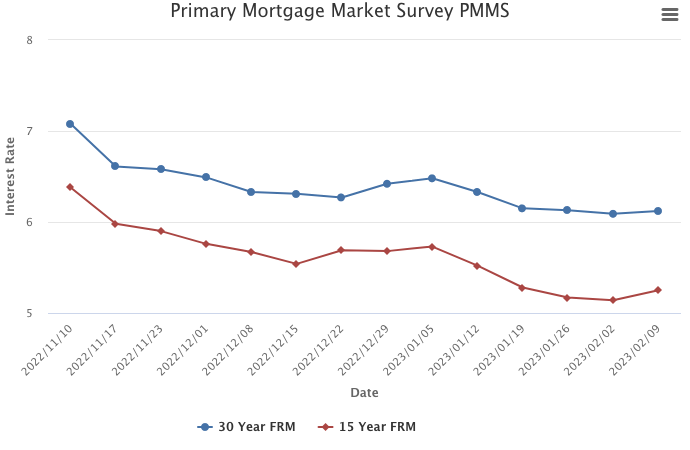

Mortgage rates moved up for the second consecutive week. The economy is showing signs of resilience, mainly due to consumer spending, and rates are increasing. Overall housing costs are also increasing and therefore impacting inflation, which continues to persist.

Information provided by Freddie Mac.

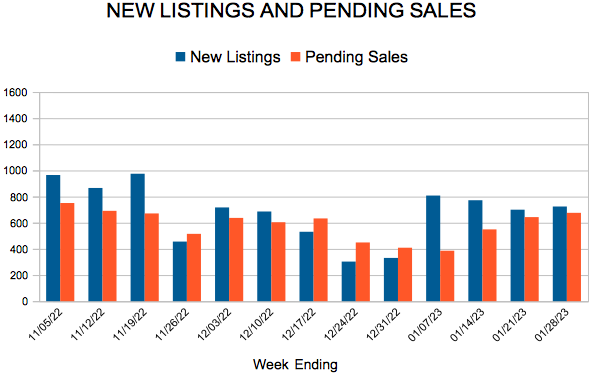

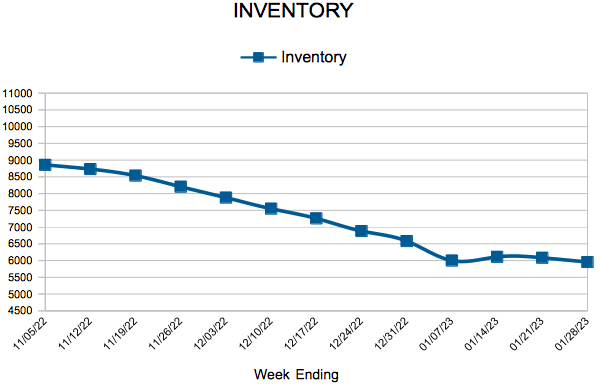

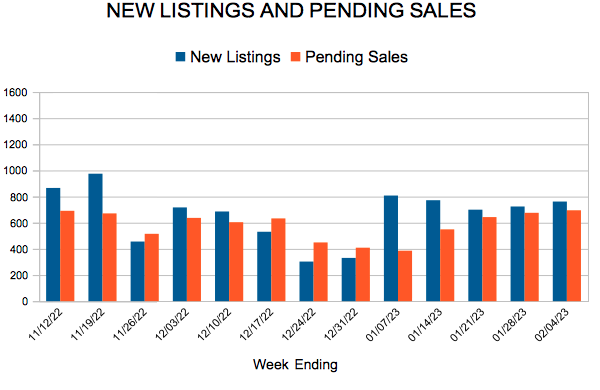

For Week Ending February 4, 2023

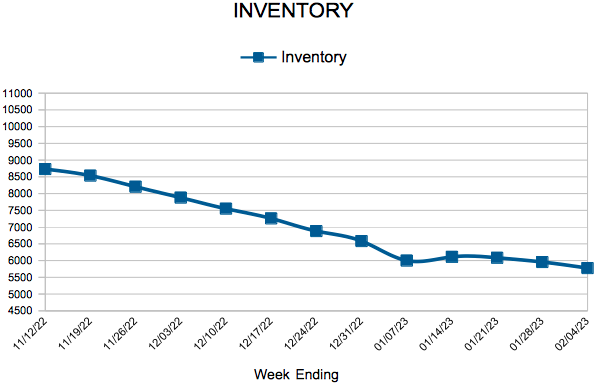

For Week Ending February 4, 2023